Actionable Steps to a Stellar Credit Score

Building Your Castle Brick by Brick: Actionable Steps to a Stellar Credit Score

Your credit score – it’s a three-digit number that holds immense power in your financial world. It can unlock the doors to lower interest rates on loans, dream apartments, and even better insurance premiums. But what if your credit score isn’t where you’d like it to be? Fear not, fellow financially faithful! This blog is your guide to building a strong credit score, brick by brick, with actionable steps you can take today.

Understanding the Credit Score Landscape

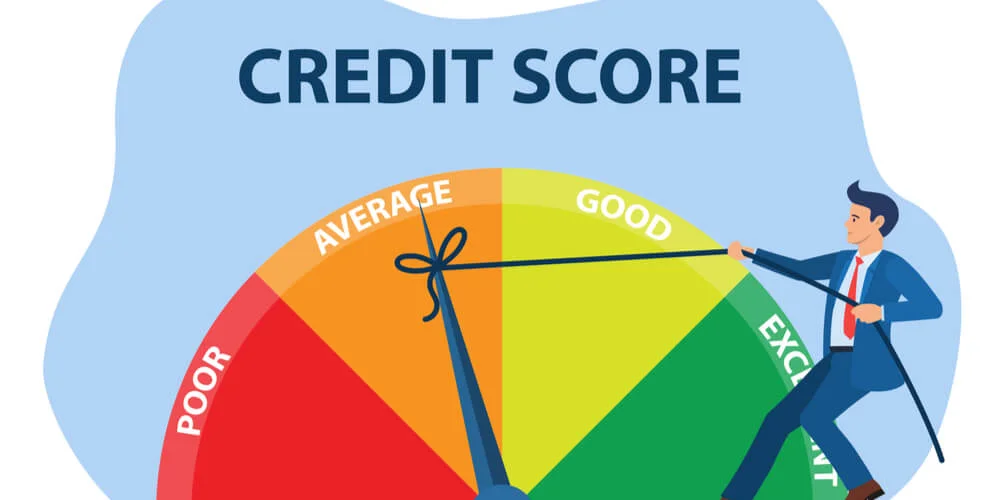

Before we delve into the nitty-gritty, let’s get familiar with the credit score playing field. In the US, Fair Isaac Corporation (FICO) is a major player, and their FICO score is widely used by lenders. Scores typically range from 300 (poor) to 850 (excellent). Here’s a breakdown of what each range generally signifies:

- 300-579: This needs work. Lenders may consider you a high-risk borrower, making it difficult to qualify for loans or get favorable rates.

- 580-669: Fair territory. You might qualify for some loans, but interest rates might be higher.

- 670-739: Good credit. You’ll have more borrowing options and potentially better rates.

- 740-799: Very good credit. You’ll enjoy even more favorable terms on loans and credit cards.

- 800-850: Excellent credit. Congratulations! You’ll qualify for the best interest rates and loan options available.

The Credit Report: Your Financial Report Card

Your credit report is a detailed record of your borrowing history, including loans, credit cards, and even past utility bills in some cases. It’s crucial to understand what’s on your report, as errors can bring down your score. The three main credit bureaus in the US are Experian, Equifax, and TransUnion. You’re entitled to a free credit report from each bureau annually. Here’s how to get yours:

- Visit Annual Credit Report

- You can request reports online, by phone, or by mail.

Step 1: Eradicate Errors – Dispute Like a Pro

Once you have your credit reports, meticulously review them for any inaccuracies. Look for things like:

- Incorrect account information: Names, addresses, account numbers.

- Late payments that you didn’t make.

- Accounts that don’t belong to you.

If you find an error, dispute it directly with the credit bureau and the creditor (bank, credit card company, etc.) that reported the information. The Fair Credit Reporting Act (FCRA) gives you the right to dispute errors and have them corrected. Here are some resources to help you with the dispute process:

- Federal Trade Commission (FTC): https://consumer.ftc.gov/articles/disputing-errors-your-credit-reports

- Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance.gov/ask-cfpb/how-do-i-dispute-an-error-on-my-credit-report-en-314/

Step 2: Become the “On-Time Bill Payer”

Payment history is the single biggest factor affecting your credit score (contributing about 35%). Make on-time payments on ALL your bills, every month. This includes credit cards, utilities, rent, phone bills, etc. Here are some tips to stay on top of your bills:

- Set up automatic payments: Many creditors offer autopay options. Utilize them to ensure on-time payments, even if you forget the due date.

- Calendar reminders and alerts: Set up digital reminders or mark due dates on a physical calendar.

- Prioritize essential bills: If finances are tight, prioritize essential bills like rent, utilities, and car payments first.

Step 3: Master the Art of Credit Utilization (Continued)

- Pay down credit card balances: Aim to pay down your credit card balances strategically. Consider focusing on cards with the highest interest rates first.

- Request credit limit increases: If you have a good payment history, consider contacting your credit card issuer and requesting a credit limit increase. This can improve your CUR without actually increasing your spending. However, be mindful of not exceeding your new limit!

Step 4: Cultivate a Diverse Credit Mix

While credit cards significantly impact your score, having a mix of credit types can also be beneficial. This might include installment loans (e.g., student loans, auto loans) alongside your credit cards. Installment loans demonstrate your ability to manage long-term debt repayment.

Step 5: Be Patient and Play the Long Game

Building a strong credit score takes time and consistent effort. Don’t expect overnight results. However, by following these steps and maintaining good financial habits, you’ll gradually see your score improve.

Bonus Tip: Become an Authorized User (Strategically)

Being added as an authorized user on someone else’s credit card with a good payment history can give your score a boost. However, this strategy comes with a caveat: their credit activity will also be reflected on your report. So, only consider this option if you trust the primary cardholder to manage their credit responsibly.

Maintaining Your Credit Score Fortress

Once you’ve built a good credit score, it’s crucial to maintain it. Here are some additional tips:

- Avoid applying for too much credit in a short period: Multiple credit inquiries can slightly lower your score.

- Monitor your credit reports regularly: Continue to check your credit reports for errors and address them promptly.

- Keep old accounts open (if possible): A long credit history with responsible management can positively impact your score. However, if an old account has a history of late payments or is associated with high fees, consider closing it after addressing those issues.

Building a strong credit score is an investment in your financial future. By following these actionable steps and adopting healthy financial habits, you’ll be well on your way to unlocking a world of financial opportunities.

Additional Resources:

- National Foundation for Credit Counseling (NFCC): https://www.nfcc.org/

- Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance