How to Get ultimate borrowing money in The USA

The Ultimate Guide to Borrowing Money in the USA

In the United States, borrowing money can be a powerful tool to achieve your financial goals. Whether you’re consolidating debt, financing a car, pursuing an education, or buying a home, understanding the different loan options and navigating the borrowing process is crucial. This ultimate guide will equip you with the knowledge you need to borrow money wisely in the USA.

Delving into Loan Options:

- Personal Loans: These versatile loans can be used for various purposes, including debt consolidation, home improvement projects, medical expenses, or unexpected costs. Personal loans are typically unsecured, meaning they don’t require collateral like a car or house. However, this often translates to higher interest rates compared to secured loans.

- Auto Loans: When purchasing a car, auto loans finance a portion of the vehicle’s purchase price. These are secured loans, meaning the car serves as collateral. Depending on your creditworthiness, loan terms, and interest rates can vary significantly.

- Student Loans: These specialized loans help finance higher education costs, including tuition, fees, living expenses, and books. Student loans can be either federal or private, with federal loans generally offering more favorable terms and repayment options.

- Home Loans: Homeownership often involves securing a mortgage, a loan specifically used to purchase a property. Mortgages are complex financial products with various options, including fixed-rate and adjustable-rate mortgages, and come with significant down payment requirements depending on the loan type and your creditworthiness.

Factors Affecting Loan Approval:

Before approving a loan, lenders assess your financial situation to determine your ability to repay the borrowed amount. Here are some key factors that influence loan approval:

- Credit Score: This three-digit number summarizes your creditworthiness based on your borrowing history, payment behavior, and credit utilization. A higher credit score generally translates to better loan terms and lower interest rates.

- Debt-to-Income Ratio (DTI): This metric compares your monthly debt obligations (minimum payments on existing loans and credit cards) to your gross monthly income. A lower DTI indicates a borrower has more disposable income to manage loan repayments and is thus considered less risky by lenders.

- Employment History: Stable employment and a sufficient income demonstrate your ability to consistently generate income to repay the loan. Lenders may consider factors like length of employment, income source, and job security.

- Loan-to-Value Ratio (LTV) (for mortgages): This ratio expresses the loan amount as a percentage of the property’s appraised value. For example, if you borrow $200,000 for a house valued at $250,000, your LTV would be 80%. A lower LTV signifies less risk for the lender and might qualify you for more favorable loan terms.

Shopping for the Best Loan Rates and Terms:

Finding the most competitive loan rates and terms requires comparison shopping. Here are some tips to navigate the loan marketplace effectively:

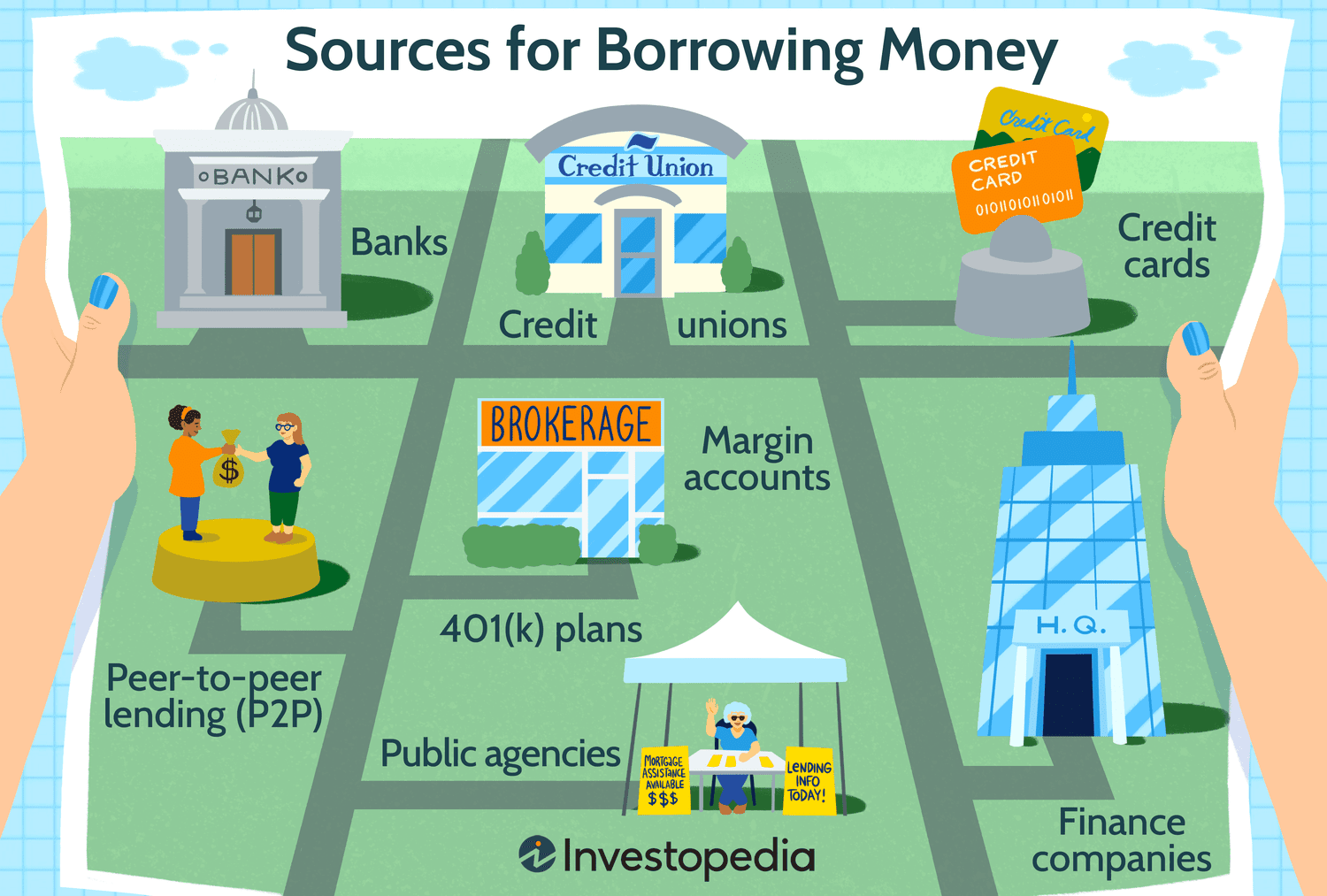

- Compare Loan Offers from Multiple Lenders: Don’t settle for the first offer you receive. Obtain quotes from banks, credit unions, online lenders, and peer-to-peer lending platforms.

- Focus on Annual Percentage Rate (APR): The APR is a more comprehensive measure of borrowing costs than just the interest rate. It includes interest, origination fees, and other charges associated with the loan, expressed as a yearly percentage.

- Consider Loan Terms: Pay attention to the loan term (repayment period), prepayment penalties (if applicable), and any other terms that might affect your financial situation.

- Pre-qualify for Loans: Pre-qualification allows you to see estimated loan terms without a hard credit inquiry that can impact your credit score. This helps you get a sense of your borrowing power and compare rates before formally applying.

- Negotiate Loan Terms: Don’t be afraid to negotiate, especially with larger loans like mortgages. A strong credit score and solid financial standing can give you leverage when negotiating interest rates and fees.

Additional Tips for Responsible Borrowing:

- Borrow Only What You Can Afford: Carefully assess your budget and ensure your monthly loan payments won’t strain your finances.

- Understand the Loan Agreement: Before signing any loan documents, thoroughly read and understand the terms and conditions, including repayment schedule, interest rate, and late fees.

- Explore Alternatives to Borrowing: For smaller expenses, consider building an emergency fund or utilizing a credit card with a low interest rate (if you can repay the balance in full by the due date) before resorting to a loan.

- Improve Your Credit Score: If your credit score isn’t ideal, focus on improving it before applying for a loan. This can involve paying down existing debt, making timely payments on all your obligations.

The Ultimate Guide to Borrowing Money in the USA (Continued)

Building upon the foundation we’ve laid, let’s delve deeper into some additional aspects of responsible borrowing in the USA:

Understanding Different Loan Types (Continued):

- Home Equity Loans and Lines of Credit (HELOCs): These borrowing options leverage the equity you’ve built up in your home. A home equity loan provides a lump sum, while a HELOC functions like a revolving credit line with a borrowing limit. Both require your home as collateral and come with risks, so careful consideration is crucial.

- Government Loans: The federal government offers various loan programs with more lenient qualification requirements and potentially lower interest rates. These programs often target specific needs, such as student loans, mortgages for first-time homebuyers (FHA loans), or loans for veterans (VA loans).

Building a Strong Credit History:

As mentioned earlier, your credit score significantly impacts loan approval and terms. Here are strategies to establish and maintain a healthy credit history:

- Obtain a Secured Credit Card: If you have limited credit history, consider a secured credit card. You provide a security deposit that serves as your credit limit, and responsible use helps build positive credit history.

- Become an Authorized User: Getting added as an authorized user on someone else’s credit card with a good payment history can positively impact your credit score, but ensure the primary cardholder has good credit habits.

- Become a Cosigner (with Caution): Cosigning a loan for someone else can help them qualify, but you’re legally responsible for repayment if they default. Only cosign for close friends or family you trust implicitly, and understand the potential risks.

- Dispute Errors on Your Credit Report: Review your credit report regularly for inaccuracies and dispute any errors you find. This can improve your credit score if corrected.

Managing Your Debt Effectively:

Responsible borrowing involves effective debt management. Here are some practices to consider:

- Develop a Budget: Create a realistic budget that allocates funds for loan repayments and avoids overspending. Prioritize necessities over wants.

- Explore Debt Consolidation: If you have high-interest debt from multiple sources, consolidating it into a single loan with a lower interest rate can simplify management and potentially save money.

- Make More Than Minimum Payments: Whenever possible, aim to pay more than the minimum amount due. This reduces your principal faster and saves on interest charges in the long run.

- Utilize Automatic Payments: Set up automatic payments for your loan obligations to ensure timely payments and avoid late fees that can damage your credit score.

Seeking Help When Needed:

Financial difficulties can happen If you’re struggling with managing debt or making loan payments, don’t hesitate to seek help. Here are some resources:

- Non-profit Credit Counseling Agencies: These organizations offer free or low-cost credit counseling and debt management plans.

- Government Assistance Programs: Depending on your financial situation, you might qualify for government assistance programs that can help with debt management or loan repayments.

Conclusion:

Borrowing money can be a valuable tool to achieve your financial goals, but it demands responsibility and informed decision-making. By understanding different loan options, the factors influencing approval, and strategies for responsible borrowing, you can navigate the borrowing process effectively. Remember, the key lies in thorough research, comparison shopping, and prioritizing your long-term financial well-being.