Types of Student Loans:

Conquering College Costs: Your Guide to Student Loans in the US

College is a springboard to opportunity, but the price tag can be daunting. Student loans are a fact of life for many students, but navigating the different options, repayment plans, and consolidation strategies can feel overwhelming. Fear not, future scholar! This guide will equip you with the knowledge to conquer college costs and make informed decisions about student loans.

Understanding Student Loans

Before diving into specifics, let’s establish the basics. A student loan is a borrowing agreement between you and a lender, typically a bank or the government. The lender provides you with money to cover college expenses, and you agree to repay the principal amount (the original loan amount) plus interest (a fee for borrowing the money) over a set period.

There are two main categories of student loans:

- Federal Student Loans: Offered by the U.S. Department of Education, these loans typically come with lower interest rates and more flexible repayment options compared to private loans. Eligibility is determined by your financial need as demonstrated by the Free Application for Federal Student Aid (FAFSA).

- Private Student Loans: Issued by banks, credit unions, and other lenders, private loans are not need-based and may have higher interest rates and stricter repayment terms.

Exploring Federal Loan Options

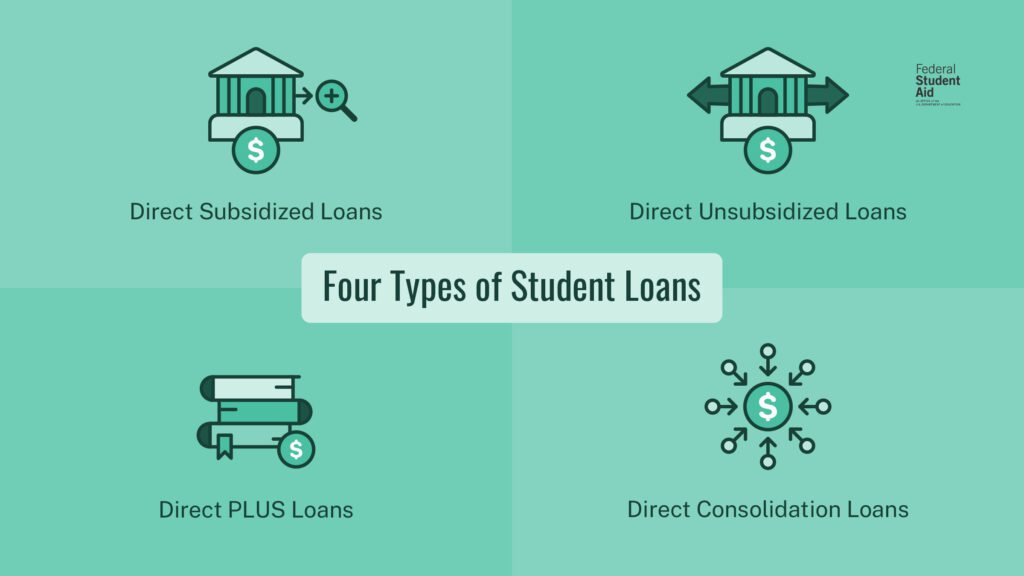

Federal student loans are a great starting point due to their borrower benefits. Here’s a breakdown of the most common types:

- Direct Subsidized Loans: Awarded to undergraduate students with demonstrated financial need. The government pays the interest on these loans while you’re in school at least half-time, during grace periods, and during periods of deferment (when repayment is temporarily postponed).

- Direct Unsubsidized Loans: Unlike subsidized loans, these are not need-based and are available to undergraduate and some graduate students. You are responsible for paying interest on unsubsidized loans from the time they are disbursed (paid out) throughout the repayment period.

- Direct PLUS Loans: Designed for graduate and professional students, as well as parents of dependent undergraduate students, to help cover the full cost of attendance minus any other financial aid received. Borrowers are responsible for paying interest on PLUS loans from the time they are disbursed.

Considering Private Loans

If federal loans don’t cover your entire financial need, private loans can bridge the gap. However, proceed with caution:

- Interest Rates: Private loan interest rates are generally higher than federal loans and can be variable, meaning they can fluctuate over time.

- Repayment Terms: Repayment terms for private loans tend to be less flexible than federal loans.

- Cosigner Requirements: Many private lenders require a cosigner, someone who agrees to be responsible for repaying the loan if you default (fail to make your payments). Choose a cosigner carefully, as cosigning can impact their credit score.

Researching and Comparing

Before accepting any loan, compare your options meticulously. Here are some key factors to consider:

- Interest Rates: Compare interest rates, including fixed vs. variable rates, to determine the total cost of borrowing.

- Repayment Terms: Consider the loan term (the length of time you have to repay the loan) and the monthly payment amount.

- Fees: Be aware of any origination fees (a one-time charge for processing the loan) or other associated fees.

- Borrower Benefits: Some loans offer benefits like interest rate reductions for automatic debit repayments or enrolling in income-driven repayment plans (discussed later).

Federal Resources for Student Loan Success

The U.S. Department of Education provides a wealth of resources to help you navigate the student loan process. Here are some key websites to bookmark:

- Federal Student Aid: [Federal Student Aid (.gov)] – This comprehensive website is your one-stop shop for all things federal student aid, including the FAFSA application, repayment options, and loan forgiveness programs.

- Student Loan Borrower Toolkit: [Student Loan Borrower Toolkit (.gov)] – This user-friendly toolkit provides information on managing your federal student loans, including repayment plans, consolidation, and deferment/forbearance options.

- National Student Loan Data System (NSLDS): [National Student Loan Data System (.gov)] – This website allows you to view a detailed report of all your federal student loans, including the loan servicer (the company that manages your loan), the outstanding balance, and the interest rate.

Demystifying Repayment Options

Once you graduate or leave school at least half-time, you’ll enter a grace period before repayment kicks in. During this time, interest accrues on unsubsidized and PLUS loans, but you are not required to make payments. When repayment begins, you’ll have a variety of federal repayment plans to choose from:

Standard Repayment Plan

This is the most common repayment plan with a fixed term (usually 10 years) and a fixed monthly payment amount. It’s a good option if you have a stable income and want to pay off your loans quickly.

- Graduated Repayment Plan: This plan offers lower monthly payments initially, which gradually increase over time. This can be helpful if you expect your income to grow in the future.

- Income-Driven Repayment (IDR) Plans: These plans tie your monthly payment amount to your discretionary income (the amount left after paying for basic living expenses). There are four IDR plans available, each with slightly different eligibility requirements and forgiveness options.

- Pay As You Earn (PAYE) Plan: This IDR plan bases your monthly payment on 10% of your discretionary income and offers forgiveness of any remaining balance after 20 years of on-time payments.

- Revised Pay As You Earn (REPAYE) Plan: Similar to PAYE, but forgiveness can occur after 10 years of on-time payments. This plan is beneficial for borrowers with high debt-to-income ratios.

- Income-Contingent Repayment (ICR) Plan: This plan bases your monthly payment on 20% of your discretionary income and offers forgiveness after 25 years of on-time payments.

- Income-Based Repayment (IBR) Plan: This plan has the lowest monthly payments based on 15% of your discretionary income and offers forgiveness after 25 years of on-time payments. However, it has the most restrictive eligibility requirements.

Choosing the Right Repayment Plan

The best repayment plan depends on your individual circumstances, such as your income, loan amount, and financial goals. Here are some factors to consider when making your decision:

- Your Current Income: If you have a low income, an IDR plan may be the best option to keep your monthly payments manageable.

- Your Expected Future Income: If you expect your income to grow significantly in the future, a graduated repayment plan could be a good choice.

- Your Desire to Pay Off Loans Quickly: If you prioritize paying off your loans quickly, a standard repayment plan might be ideal.

- Your Eligibility for Loan Forgiveness: If you work in a public service job, you may qualify for Public Service Loan Forgiveness (PSLF) and should choose a plan that qualifies for forgiveness, such as PAYE or REPAYE.

Exploring Deferment, Forbearance, and Cancellation

In certain situations, you may be able to temporarily postpone or reduce your loan payments. Here are some options to consider:

- Deferment: This allows you to temporarily postpone loan payments while meeting specific eligibility requirements, such as enrolling at least half-time in school or experiencing financial hardship. Interest continues to accrue on unsubsidized and PLUS loans during deferment.

- Forbearance: Similar to deferment, forbearance allows you to temporarily postpone or reduce your loan payments. However, unlike deferment, interest continues to accrue on all types of federal student loans during forbearance.

- Cancellation: Under specific circumstances, your federal student loans may be cancelled. This can occur due to permanent disability, school closure, or if you work in a public service job and qualify for PSLF.

Consolidation Strategies

If you have multiple federal student loans, consolidating them can simplify your repayment process. Consolidation combines your loans into a single loan with one interest rate and one monthly payment. This can be helpful if you’re juggling multiple loans with different servicers and interest rates. However, consolidation may not always be the best option. Here are some things to consider:

- Loss of Income-Driven Repayment Benefits: If you’re currently enrolled in an IDR plan, consolidation may disqualify you from that plan’s specific forgiveness benefits.

- Increased Loan Term: Consolidation can extend the repayment term of your loans, which means you’ll end up paying more interest in the long run.

Life After Graduation: Managing Student Loans Effectively

Successfully managing your student loans requires a proactive approach. Here are some tips to stay on top of your debt:

- Enroll in Automatic Debit Repayment: This ensures your monthly payments are made on time and can qualify you for a small interest rate reduction on some federal loans.

- Set Up a Budget: Include your student loan payment in your monthly budget to ensure you have enough money allocated for repayment.

- Explore Additional Repayment Options: If you receive a significant raise or come into a windfall, consider making additional payments towards your principal to reduce your loan balance faster.

- Stay Informed: Changes to federal student loan programs and repayment options occur periodically. Stay informed by checking the Department.